Case for higher global equities allocation in SMSF

- Fri 29 November 2019

As interest rates fall, Australians must look beyond familiar asset classes.

This year has been historic for the Reserve Bank of Australia. It moved to an easing bias shortly after the federal election in May and has reduced the cash rate for the third time in five months.

As well as the current 0.75 per cent being a record low Australian cash rate, Australia now has the equal sixth-lowest rate in the world and is on par with the United Kingdom, an economy grappling with Brexit-induced uncertainty.

The fall in the cash rate reflects the RBA’s concern about its ability to meet an inflation target of between 2 and 3 per cent on average over time. In cutting rates so aggressively this year, the RBA is hoping to generate a stronger labour market and higher wages growth and stimulate domestic consumption.

Fortunately for the RBA, the transmission mechanism of monetary policy works well in the Australian economy, as around 80 per cent of housing loans and most business loans have variable interest rates.

Households and businesses should receive an economic windfall almost immediately, while a weaker Australian dollar should support export-oriented and import-competing sectors.

Chart 1: Central bank interest rates

Source: Fidelity International, Bloomberg, October 2019

While lower lending rates are generally good for those who want to borrow, lower deposit rates reduce the incentive for households to save. Instead, there is increased incentive for households to spend money on goods and services.

The question is whether households will respond to a new world or ultra-low interest rates by borrowing and spending more, or they choose to pay down debt in an economy that has the second highest level of household debt to GDP in the world.

Lower rates also support asset prices (such as housing and equities) by encouraging demand for them. Higher asset prices also increase the equity (collateral) of an asset that is available for banks to lend against. This can make it easier for households and businesses to borrow.

An increase in asset prices increases people's wealth. This can lead to higher consumption and housing investment because households generally spend some share of any increase in their wealth.

The RBA has not been the only central bank to cut interest rates in 2019. In total, 45 central banks, including the US Federal Reserve, the European Central Bank and across the emerging and developing world, have reduced rates to stimulate their respective economies.

In an environment where global interest rates are plumbing record lows, investors – from large sovereign wealth funds to small private investors – are increasingly likely to hunt for higher-return assets to generate superior performance for their investment portfolios (the “portfolio rebalancing effect”).

Chart 2: Fidelity International capital market assumptions

Source: Fidelity International, 30 June 2019, reflecting data for second-half 2019. All returns in Australian currency These estimates are based on Fidelity International’s proprietary modelling for illustrative purposes only and reflect the views of its investment professionals. Inflation is an average of projections of Fidelity’s investment professionals, based on CPI.

Hunt for yield

Australians are now in the same boat as many international investors in their search for new investment opportunities.

Not too long ago, Australians could hold defensive assets such as cash and government bonds, and the interest earned would be enough to protect their wealth from the eroding effects of inflation. Today, if an investor wants to generate superior returns they must look further afield than traditional investments such as term deposits and Australian equities.

Australian equities are a popular choice for investors, currently making up the largest share (38 per cent) of self-managed superannuation funds (SMSFs) under management. But by limiting your portfolio to domestic shares you are missing exposure to a huge number of the world’s most successful companies. Global equities can also offer diversification and significant returns from regions and industries positioned for growth.

An allocation to both Australian and global equities can bring investors a broader choice of investment opportunities. Importantly, this blended approach to equities can also reduce volatility and enhance potential portfolio returns. Because assets do not always have a strong correlation to each other, global and Australian equities can both play an important role in diversifying the overall risk of the portfolio.

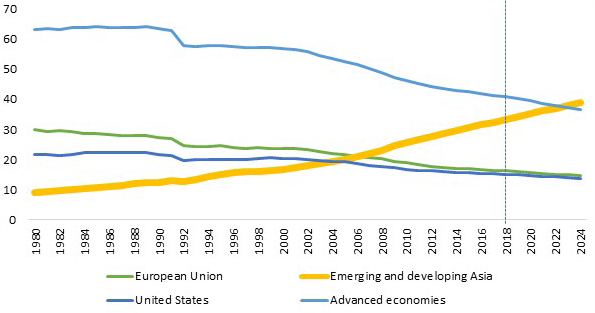

Looking further afield, emerging markets have been growing rapidly in recent years and now represent nearly 60 per cent of global growth and more than 50 per cent of global GDP. Emerging and developing Asia alone is expected to be larger than all the advanced economies combined by 2022.

Once dominated by agriculture and cheap manufacturing, emerging market countries are now home to some of the world’s fastest-growing economies and most innovative companies.

Chart 3: Asia will be larger than all of the developed markets around 2022

Source: Fidelity International, IMF, October 2019. For illustrative purposes only.

Emerging market equities do not just offer Australian investors growth potential; they also increasingly offer genuine diversity and possible protection from an economic downturn in the developed world. Of course, proximity to these markets is important to be able to assess the risks. That is why we place so much emphasis on bottom-up, fundamental research.

Fidelity believes an active investment approach offers crucial advantages for investors because it allows the investment team to select opportunities from a much broader universe than those available in the index. The advantage to investors is also in greater diversification across countries, sectors and companies, which helps reduce risk and, importantly, provides more opportunities to create meaningful value.

As we approach a new decade, global monetary policy developments are challenging investors across the globe to reassess their investment portfolios and goals. For Australian investors to be successful, looking further than the traditional asset classes will be required.

About the author