Three top tips for 2022

- Fri 03 December 2021

Beware market hype, seek good management and favour strong balance sheets.

The month of January takes its name from Janus, the ancient Roman god of beginnings and endings. He is usually depicted with two faces, one looking forward and one looking back.

Similarly, as the year draws to a close, we always find ourselves looking forward with anticipation to a new year. For financial markets this typically means opinions on what to expect in 2022, with many putting out year-end S&P/ASX 200 targets (although few mark their homework 12 months later!), and various articles highlighting the key risks or themes to watch out for in 2022.

However, after a period of bushfires, a pandemic closed borders, and months of lockdown that has coincided with one of the fastest periods of house and share price growth in history, I’ve been left with a dose of scepticism in the value of my crystal ball.

So just like Janus, perhaps at this time of year, we should dedicate at least as much time looking back as forward, asking ourselves the question: What have we learnt from 2021 that might be relevant for 2022?

If the word of the year (roughly defined as a word you never want to hear again by year-end) for 2020 was “unprecedented”, I would argue 2021’s word has been “inflation”. November’s US CPI (consumer price index) print of 6.2% for the 12 months to October was the highest such reading since 1990, and the sixth consecutive month where the CPI rose more than 5% for the 12-month period.

On 1 Jan 2021, the US 10-year government bond was yielding 0.93%. As of mid-November, it was yielding 1.63% – nearly double. Similarly, the Australian 10-year yield has leapt from 0.97% to 1.84% over those months.

Company after company globally has painted a picture of extreme supply disruptions, product shortages, soaring input costs and tight labour markets. Over this period, the dominant debate raging in financial markets has been whether this inflation is transitory, as supply chains normalise post-pandemic, or whether it is structural.

Here are three lessons from 2021 to take in 2022:

Lesson #1: Beware the dominant market narrative

Although time will clearly settle this debate, the lesson from 2021 (and the past few years) is to beware the dominant market narrative.

Despite markets correctly anticipating rising inflation that indeed occurred over 2021, the ASX 200 has risen against this backdrop by a healthy 11% in the year to mid-November. Does this mean inflation doesn’t matter for equities? No. It means that trying to pick the eyes out of where these big macro drivers (e.g. inflation and interest rates) are headed is a fool’s errand: you’re as likely to be wrong as right, and then just as likely to be wrong about what it means for markets.

Every year a dominant market narrative will emerge. Some seem quaint in hindsight. Remember in 2012 when we worried about the level of Greek government debt? Other narratives can have a similarly large and rapid impact on markets. The March 2020 global drawdown reflected a market that took 23 days to price in that the coronavirus pandemic would cause a global solvency crisis, with the ASX 200 falling 35% off its highs before another narrative quickly emerged: central banks will save us.

The reason to be wary of the dominant market narrative is because it rarely matters in the long run; however, it can “scare” people out of owning good, solid businesses.

If you’d simply fallen asleep on 1 Jan 2020 and woken up in late 2021, with your money invested in the ASX 200 over that time, your holding would be worth about 15% more including dividends, translating to roughly 7% per annum (which is interestingly around the long-term average return of Australian equities over many decades). You might conclude that you’d missed little in your slumber!

In the long run, only one thing drives the value of a company, and that is the returns it generates on the capital invested in the business.

Lesson #2: Own businesses with good balance sheets

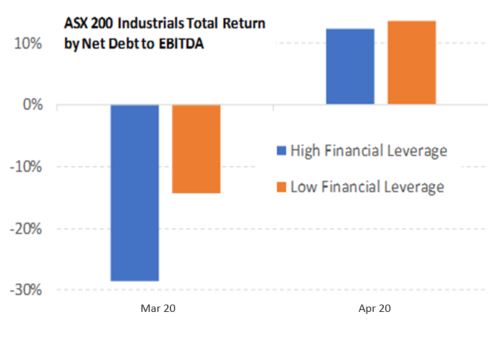

Every year, Airlie would advocate owning businesses with solid balance sheets. For one thing, it provides protection in a sharp market drawdown, as seen last March (and highlighted in the chart below), those businesses with lower levels of gearing (debt to equity) fared much better through the March slump.

Figure 1: ASX200 Industrials total shareholder return

Source: MST Marquee, Airlie Research

The other reason we like a strong balance sheet is that optionality is a source of value upside, something we saw repeatedly over 2021.

In our view, the market is typically terrible at putting a value on the optionality that a solid balance sheet provides unless it is forced to through a capital management event. This may occur through the announcement of a surprise special dividend (à la Wesfarmers with a $2 per share capital return announced in August), significant buybacks such as those undertaken by the big four banks in 2021 (partly underpinning a 25% average total shareholder return for the big four to mid-November), or a cash- or debt-funded acquisition (e.g. Nick Scali Furniture has rallied 35% since it announced the acquisition of Plush Sofas, largely funded through its cash balance).

The good news for 2022 is that the past two years have strengthened many balance sheets, with strong demand and capital expenditure cuts driving lower levels of gearing.

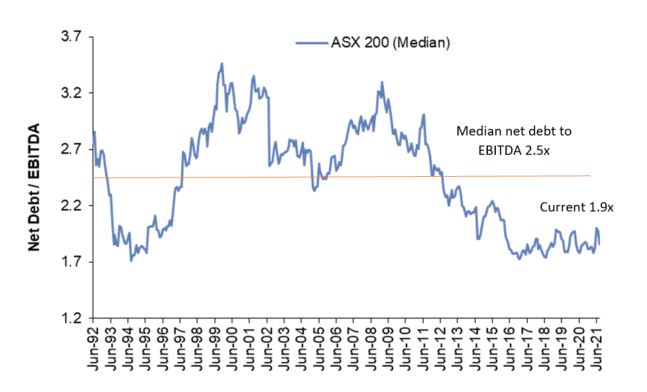

As per the chart below, corporate gearing for the ASX 200 is well below its long-term median of 2.5 times net debt to EBITDA (earnings before interest, tax, depreciation, and amortisation). We expect this latent optionality to fuel further capital returns to shareholders over 2022.

Figure 2: Median net debt to EBITDA of ASX200

Source: Goldman Sachs, Airlie Funds Management.

Lesson #3: Management matters

This past year gave us more evidence that management matters, not only for creating value for shareholders but by giving us further examples of how a poor management team can destroy value.

Sadly, every year we seem to get a scandal that reminds us of this: from AMP charging fees to dead customers, to the destruction of culturally significant sites at Rio Tinto, to operational and governance issues at Crown Resorts.

In Airlie’s opinion, management scandals are yet another reminder that backing businesses that are run by talented and ethical people is an important consideration in investing.

In conclusion, in anticipating the outlook for Aussie equities next year, we advise looking back to look forward. 2021 was another year that reinforced the value of looking through the short-term noise, instead of focusing on investing in well-run companies with solid balance sheets.

About the author

More Investor Update articles

Outlook for global equities

Risks rising amid higher inflation and record exposure in the US to shares and debt.

The views, opinions or recommendations of the author in this article are solely those of the author and do not in any way reflect the views, opinions, recommendations, of ASX Limited ABN 98 008 624 691 and its related bodies corporate (“ASX”). ASX makes no representation or warranty with respect to the accuracy, completeness or currency of the content. The content is for educational purposes only and does not constitute financial advice. Independent advice should be obtained from an Australian financial services licensee before making investment decisions. To the extent permitted by law, ASX excludes all liability for any loss or damage arising in any way including by way of negligence.