What’s unique about Australian bond futures?

- Tue 31 May 2022

- 3 MIN READ

The first article in the ASX series on the Australian bond futures market explores the benefits of futures, the differences between Australian and offshore markets, and why ASX Bond Futures rank among the top three interest rate futures contracts globally.

Australian bond futures are financial derivative products designed for investors trading and hedging medium to long-term Australian dollar interest rates. Due to the way they are structured, they offer several advantages, the most recognised of these being the liquidity and transparency they provide.

According to Helen Lofthouse, Group Executive of Markets at ASX, the importance of futures to the functioning of debt markets has been more apparent than ever during the COVID-19 crisis.

“During periods of market stress, we tend to see liquidity migrate back towards the key bond futures contracts from both the physical bond and swap market,” Lofthouse says.

“At the height of the pandemic in 2020, OTC markets went through a period of illiquidity. In contrast, bond futures continued to provide liquidity at tight bid offer spreads. It became clear to us that the futures market was the primary point of price discovery for multiple markets.”

As Australian Office of Financial Management (AOFM) CEO Rob Nicholl explains, “The futures market experiences significantly higher turnover than the underlying Treasury bond market. For this reason, ASX Bond Futures offer an important reference point in the pricing of capital market instruments and management of interest rate risk.”

Due to this important function, and some unique approaches taken in Australia, ASX Bond Futures consistently rank among the top three most liquid interest rate derivatives in the world in terms of volume traded[*], ranking with the likes of global giants CME and Intercontinental Exchange. This is impressive for a country that historically ranks around 14th in GDP.

Keeping it simple

The Australian bond market has a unique pricing structure compared with major offshore markets. The popularity of ASX Bond Futures also makes for easy trading, with participants able to move in and out of sizeable positions across time zones and often at the minimum bid offer increment.

In fact, Lofthouse suggests that having simple, accessible products is one of the main drivers behind ASX’s global appeal.

“A key difference of our bond market is that AUD bonds trade on the basis of yield as opposed to capital price,” she says.

“Our futures follow the same structure, which in turn makes them more intuitive and easy to trade when compared with other markets.”

ASX Bond Futures are quoted and traded as 100 minus the yield to maturity, making the yield transparent and easy to compare to cash market instruments.

An important by-product of this convention is that the tick value, or dollar value per basis point (also known as DV01) is variable and will change in accordance with movements in the underlying interest rate. For all contracts, the tick value will decrease as interest rates increase and vice versa, meaning the future will always reflect the convexity of the yield curve and the current DV01.

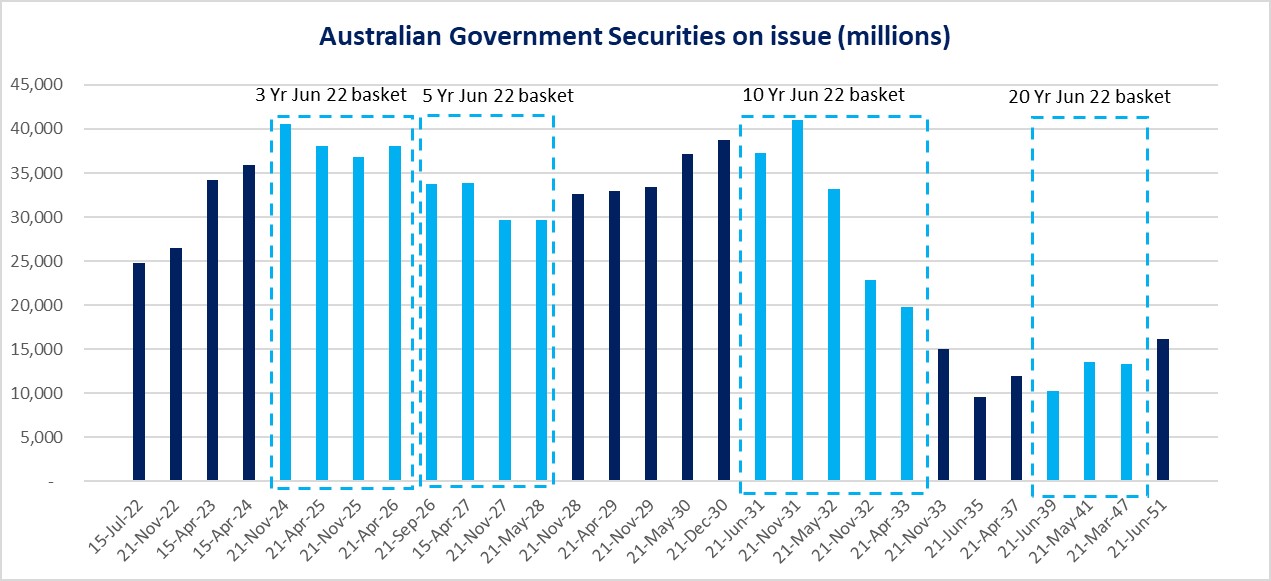

Another unique feature is cash settlement. ASX Bond Futures are cash settled on a quarterly basis. Each futures contract is underpinned by a basket of liquid Australian Government Securities (AGSs), with the quarterly settlement price calculated as an average of the price of the basket at the time of expiry.

In contrast, most offshore bond futures are deliverable. In a deliverable market, a buyer who holds an open position at expiry of the futures contract is required to take delivery of a physical bond from the seller. The seller will typically choose to deliver the cheapest or most cost-effective bond in the basket. Cash settlement bypasses this whole process by simply requiring the transfer of cash between buyers and sellers at expiry, based on the difference between the prior day’s settlement price and the expiry settlement price.

As there is no requirement to access the underlying cash bond market, there are no restrictions on who can trade and hold positions to expiry, opening the market to a broad range of users.

A new point on the curve

ASX lists bond futures at key maturity points along the yield curve to support the structure and needs of the underlying bond market.

In November 2020, a new 5 year bond future was launched to bridge the gap between the long-established 3 and 10 year bond futures.

“We saw there was a need for an additional point on the curve,” says Lofthouse.

“With increased issuance of government bonds in response to the pandemic, the volume of mid-curve bonds grew substantially compared to just a few years prior. In addition to this, the RBA had anchored the 3 year bond yield at the cash rate, making it a less effective hedge for those mid-curve exposures.”

ASX now lists bond futures at 3, 5, 10 and 20 year maturities, covering the full spectrum of government bonds on issue.

Australian Government (Commonwealth Treasury) bonds on issue

Reference data: AOFM and ASX

In addition to providing a better hedge, the 5 year contract introduces new relative value trading opportunities with US, UK, Canadian and European markets all offering 5 year bond futures.

“Having a 5 year future provides additional structural support for the AGS market,” says Nicholl. “It also creates new trading opportunities and should help to increase investor interest and liquidity in the mid part of the curve.”

The contract has traded over 1.9 million lots since launch, with average Open Interest at 52,000. ASX’s aim is to turn the 5 year future into an established futures contract that sits alongside the existing 3 and 10 year futures in terms of liquidity and turnover. Part of the challenge is getting liquidity to shift from the long-established 3 and 10 year contracts, a behaviour that is not easy to change.

Lofthouse, however, believes it will eventually happen.

“With just over $300 billion in bonds now sitting between the 3 and 10 year futures, a 5 year futures contract may be a sensible option,” she says.

“We know it is generally a better hedge for mid-curve exposures. We know the market is supportive. It’s only a matter of time before we could see that migration of liquidity.”

Future articles

The second article in our Australian bond futures market insight series will address bond and swap ‘exchange of futures for physicals’ (EFPs) and how to incorporate EFPs in trading strategies. A third article will delve into the dynamics of the quarterly bond roll.

[*] World Federation of Exchanges Derivatives Report 2020