Long butterfly

The long butterfly can be used to generate extra income when the investor believes the market is stagnating but does not want exposure to an unexpected rise or fall.

Long butterfly

The long butterfly can be used to generate extra income when the investor believes the market is stagnating but does not want exposure to an unexpected rise or fall.

| Market outlook | Neutral |

| Volatility outlook | Falling |

| The long butterfly | |

|---|---|

| Construction | long call X, short 2 calls Y, long call Z |

| Point of entry | market near central strike Y |

| Breakeven at expiry | X plus cost of strategy Y less cost of strategy |

| Maximum profit at expiry | central strike less lower strike less cost of spread |

| Maximum loss at expiry | cost of strategy |

| Time decay | market around central strike: helps market around upper or lower strike: hurts |

| Margins to be paid? | yes |

| Synthetic equivalent | various (see below) |

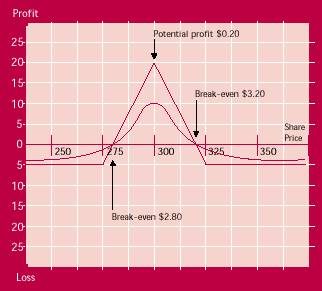

The maximum profit from the long butterfly will be earned if the market finishes at the middle strike price at expiry. In this case, only the lower strike price call will finish in the money. Accordingly, the trader will profit on the difference between the middle and lower strike price, less the cost of the spread. Most of this profit will develop in the last month as time decay accelerates. The most the trader can lose is the cost of the spread, which will occur if the market finishes out past either 'wing' of the long butterfly.

If the share price remains steady, the position may be left until close to expiry since the profit develops almost entirely in the last month.

If the share price moves sharply up, the trader may consider liquidating the position in order to avoid exercise. If the share price moves sharply down, the trader may close out in order to salvage some time value from the taken legs of the strategy.

As outlined above, the long butterfly can be constructed using only calls. However, there are several alternate ways to set up this strategy. These include:

The decision as to how to construct the long butterfly will be influenced by several factors.

The cost of the strategy may vary depending on the component options used. The trader may need to examine the most economical way of entering the position.

The liquidity of the various series of options should be considered as the long butterfly may be difficult to trade at the best of times.

While the use of the long butterfly implies a neutral view of the market's direction, any leaning towards bullishness or bearishness will influence the choice of component options. Since the strategy always involves the sale of options around-the-money, there is always the risk of exercise as the market price moves away from the central strike price. Whether this risk is present in the case of a market rise or a market fall, will depend on whether calls, or puts, or a combination of the two, have been sold. If the trader has built the long butterfly using only calls, a rise in the market introduces the risk of exercise. If only puts have been used, a fall in the market exposes the trader to the same risk. Therefore, any directional view of the market the trader holds may suggest one way of structuring the long butterfly in preference to another.

The second of the three alternatives listed above suggests the long butterfly can be thought of as an extension of the short straddle. The outer wings act as protection in case of a sharp move in the market. A sharp market move can be devastating to the short straddle, whereas the loss is limited for the holder of a long butterfly. Once the stock price moves beyond the strike price of one of the outer legs, the trader is protected from any further loss.

It is now December. You believe that shares in XYZ Limited are likely to remain steady for a couple of months and wish to derive some income during this period. You consider selling a straddle but are concerned that an unexpected break either way in the market could be very damaging. You decide to use the long butterfly in order to limit the loss you would face in the event of such a move.

Buy 1 Feb $2.75 Call @ $0.45

Sell 2 Feb $3.00 Calls @ $0.27

Buy 1 Feb $3.25 Call @ $0.14

The information contained in this webpage is for educational purposes only and does not constitute financial product advice. ASX does not represent or warrant that the information is complete or accurate. You should consider obtaining independent advice before making any financial decisions. To the extent permitted by law, no responsibility for any loss arising in any way (including by way of negligence) from anyone acting or refraining from acting as a result of this material is accepted by ASX.

Both courses have 10 modules with each module taking 20-25 minutes to complete

Complete suite of online courses from beginner to advanced options education plus trading courses on technical analysis and trading systems. (Free Sign-Up)

Two monthly trading webinars designed for you to ask questions live while presenters walk through an introduction to options and advanced options trading. (Free Sign-Up)

Challenge your knowledge of options and sharpen your trading skills.

Next game starts 15 June and ends on 17 July 2020.