Market quality highlights from the 3-Year Treasury Bond Futures tick size change

- Mon 15 December 2025

- 5 MIN READ

In July 2025, ASX re-established the 3-Year Treasury Bond Futures contract minimum price movement ('tick size') to 0.5 basis points. This targeted microstructure change was informed by comprehensive analysis of order book dynamics and industry feedback. Since implementation, ASX has observed a notable uplift in liquidity, with top of book volume increasing by an average of 75% compared to the pre-change 2025 average, alongside sustained average volumes across the top 5 price levels. These enhancements have delivered more efficient execution conditions, supporting improved trading and risk management outcomes for market participants.

Introduction

The 3-Year Treasury Bond Futures contract tick size change was implemented following an industry consultation and market quality review that found market conditions had stabilised and were once again suited to a finer 0.5bp increment. This adjustment follows the temporary widening to 1bp introduced in October 2022 after the end of RBA Yield Curve Control (YCC) that drove heightened volatility and impacted market liquidity. The reinstatement reflects ASX’s ongoing role in monitoring market conditions and calibrating contract settings to ensure they remain aligned with prevailing trading behaviour and liquidity dynamics.

Tick size plays a fundamental role in the microstructure of interest rate futures. It is one of the key levers available to ASX when assessing contract specifications that influences how liquidity forms, how spreads behave and how efficiently participants can trade. Determining the optimal tick size includes balancing liquidity and price discovery, where a tick that is too large can increase execution costs for participants, while one that is too small can fragment liquidity across the order book.

For the three-year contract, as a key benchmark derivative product in the Australian market, an appropriate tick size setting is particularly critical for maintaining efficient trading and to continually support effective hedging outcomes.

Since reinstating the 0.5bp tick, the 3-Year Futures contract has shown improved top of book liquidity when compared on a like for like basis with the 1bp level while maintaining resilience across the broader order book, with consistent depth observed within the top 5 price points.

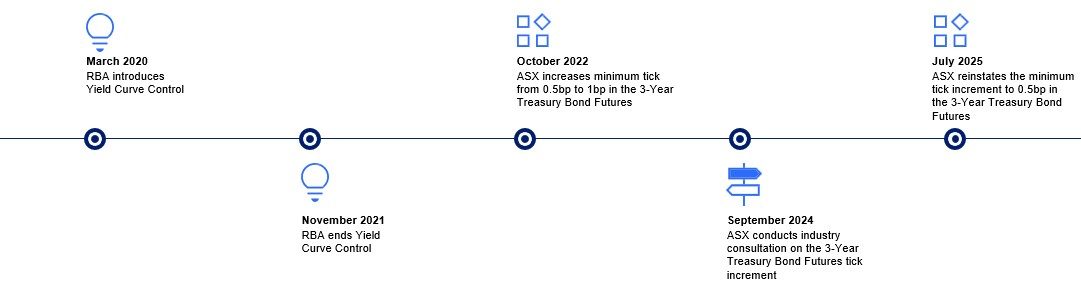

Market conditions leading to the 2022 Tick widening

In March 2020, the RBA introduced Yield Curve Control (YCC), purchasing government bonds to pin the three-year yield at 0.25% and later 0.1% as part of its monetary stimulus response to the economic disruption caused by COVID-19. When YCC ended in November 2021, the 3-Year market experienced a notable increase in volatility where price movements became less predictable and resultingly, confidence from market participants to provide resting liquidity in the order book declined. ASX did not widen the tick immediately after YCC ended, but only after observing a sustained period of market volatility, which degraded market quality as evidenced by reduced market liquidity and therefore impacted the ability for market participants to efficiently use the contract for hedging and risk management purposes. The subsequent move to a 1bp tick in October 2022 restored market confidence, rebuilt open interest and encouraged broader participation in the 3-Year Futures contract as ASX had anticipated.

Independent analysis published by the Reserve Bank of Australia in the research discussion paper, Back to the Futures: Liquidity in Australian Bond Futures amid Market-Moving Events since COVID-19 authored by Finlay, Jackman and Titkov 2025, further validates that the October 2022 shift to a 1bp tick led to an increase in market depth and lower price impact, returning towards the levels seen in 2019 prior to the onset of COVID. The authors concluded that this market structure change improved liquidity outcomes during this period (Finlay, Jackman and Titkov, 2025 pp15/50).

Importantly at the time, ASX indicated that the 1bp tick size was a temporary measure, outlining certain target improvements in market conditions that needed to be achieved, before reverting to 0.5bps. In 2023 and 2024, trading conditions showed signs of recovery and the liquidity thresholds set by ASX as prerequisites for returning to the smaller tick size were met and sustained when assessed against pre-pandemic levels. This was evidenced in the 2024 ASX 3 Year Treasury Bond Futures Minimum Tick Increment Consultation Paper which highlighted that order book depth (up to 5 price points) and top of book levels in 3-Year Treasury Bond futures had regained pre-pandemic consistency, averaging 3,200 lots in Q2 2024. Additionally, night session volumes in the contract were elevated compared to pre-pandemic norms, averaging 40% of total volume between Q3 2023 to Q2 2024), versus 30% prior to the pandemic.

Timeline

Observed outcomes since the 3-Year Bond Futures Tick Change

1. Strengthened top of book liquidity

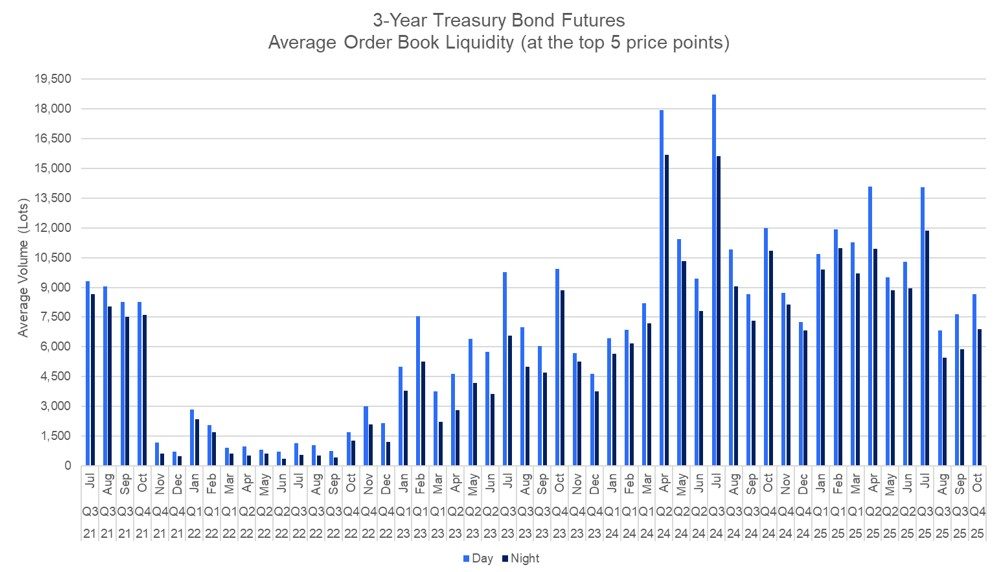

Since reinstating the 0.5bp tick size effective trade date 21 July 2025, the 3-Year Treasury Bond Futures contract has exhibited a steady uplift in top of book liquidity. Importantly, because the narrower tick distributes liquidity across a greater number of price points, post-change depth is assessed on a like-for-like basis by aggregating the top 2 levels (a 1bp equivalent band) from the night session when the change was first introduced.

Based on 2025 year-to-date observations, liquidity within this 1bp equivalent range has increased notably across both day and night trading sessions. Given the timing of the implementation, analysis of post-change behaviour is conducted from August onward, the first full month under the 0.5bp tick. In the day session, average liquidity was 2,200 lots in January to June and rose to 3,600 lots between August and October, resulting in a 64% uplift. Night session liquidity followed a similar pattern, strongly increasing by 85% over the same comparison period, with average top of book liquidity rising from 1,300 lots to 2,400 lots post-implementation. In comparison, the 10-Year Treasury Bond Futures contract, with no microstructure change applied, showed an uplift of approximately 45% in top of book liquidity over the same analysis period (January to June vs August to October), across both day and night sessions.

Source: ASX data

Source: ASX data

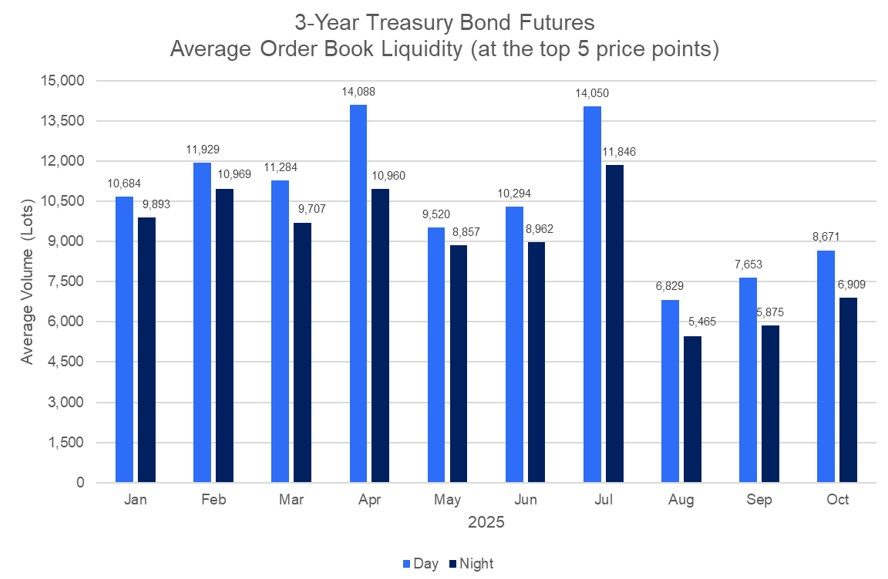

2. Improved order book depth

Following the tick size adjustment, order book depth at the top five price levels now represents a 2.5bp price range compared to the previous 5bp (under a 1bp tick increment) where order book depth has remained resilient and robust, despite the change. A comparison of the August to October periods in 2021 and 2025 – both operating under a 0.5bp tick size, has highlighted that day session order book depth at the top 5 price levels has remained broadly unchanged, holding at an average of 8,000 lots daily across the three months in both years. Night session depth shows only a modest decline, falling from approximately a monthly average of 7,700 lots to 6,100 lots during the same analysis period. This provides a useful benchmark for market conditions that remove the volatility associated with the RBA’s quantitative easing measures that came into effect November 2021.

Source: ASX data

Additionally, from a year-to-date perspective, order book depth has continued to be comparatively strong. Prior to the tick size change, day session order book depth at the top five price points ranged between an average of 9,500 to 14,100 lots between January and June, with night session averages between 8,900 to 11,000 lots. Whilst the price range has halved after the tick size change, order book depth has remained relatively resilient at an average range of 6,800 to 8,700 lots during the day trading sessions. This is a positive outcome as the market has adapted to the updated tick increment and continues to be sufficiently liquid at multiple price points.

Source: ASX Data

Conclusion

In conclusion, setting the tick increment for the 3-Year Treasury Bond Futures contract has led to measurable improvements in liquidity and overall market quality. The sustained resilience of order book depth and the marked increase in top book volume highlight the effectiveness of this targeted adjustment. As market conditions continue to evolve, ongoing monitoring and engagement with participants will remain essential to maintaining effective contract settings and supporting a robust, efficient market.

About the author

Disclaimer

Information provided is for educational purposes and does not constitute financial product advice. You should obtain independent advice from an Australian financial services licensee before making any financial decisions. Although ASX Limited ABN 98 008 624 691 and its related bodies corporate (“ASX”) has made every effort to ensure the accuracy of the information as at the date of publication, ASX does not give any warranty or representation as to the accuracy, reliability or completeness of the information. To the extent permitted by law, ASX and its employees, officers and contractors shall not be liable for any loss or damage arising in any way (including by way of negligence) from or in connection with any information provided or omitted or from any one acting or refraining to act in reliance on this information.

© Copyright ASX Operations Pty Limited ABN 42 004 523 782. All rights reserved 2025.